Russian-Ukraine War & the Corn Market

So, there are a lot of numbers flying around in the daily news wires surrounding Russia and Ukraine's affect on the global corn and wheat market. The values are quoted in million metric tons, billion bushels, million bushels and sometimes percentages. I work with numbers every day and even I find it difficult to keep everything straight. So, I’ll attempt to give the gist of the situation and leave the numbers out.

- Ukraine only accounts for 3.5% of total world corn production, but they export 80% of what they produce! Combined, Russia and Ukraine are projected to account for roughly 18% of total world corn exports and 29% of global wheat exports.

The issue is that Ukraine cannot export any commodities right now because they rely on the Black Sea to do so, and the Black Sea is well, out-of-commission. This puts a lot of countries in a bind because they rely on Ukraine for food. Major corn importing countries, particularly in the Middle East and North Africa, are reducing how much corn they are using and relying on existing stocks; however, they can only do that for so long. Therefore, they must rely on the US and South America for supplies. This is largely because Brazil, Argentina, Ukraine, and the US are projected to account for 85% of global exports.

The trouble is that while Brazil and Argentina’s new crop supplies are forecast to be record-high in their marketing year, their corn supplies will not be available to the world market for another few months. So, as the world’s largest and residual supplier of corn, the US can fill the gap until South American exports are fully online; however, it comes at a cost. According to the International Grains Council, US corn export prices are record high (figure below from USDA FAS).

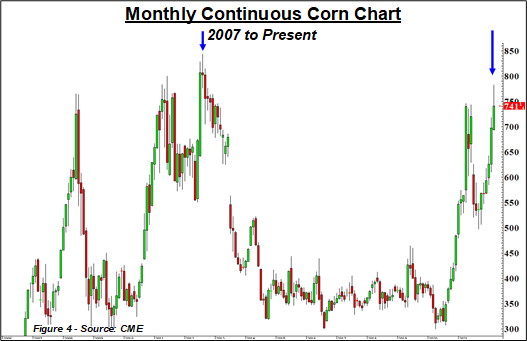

The Russian-Ukraine situation compounded the rally in prices from last year. On the heels of ravenous Chinese demand and reduced available supplies in Brazil, the front-month corn futures market reached a high of $7.4625/bu. in April 2021 before correcting $2+/bu. lower in the fall. Then, the Russian-Ukraine war and massive speculation fueled prices higher. On March 4th, the corn market came within $0.60/bu. of the all-time highs posted in August 2012.

The previous two years of bullish inputs, extreme uncertainties, and black swan events ensure that this coming crop year will be unlike any other. Domestically, we’re dealing with a tightening carryover, high input costs, and stiff competition for acres. Globally, South America is fighting drought, and Ukraine’s prospects for an exportable corn supply is ominous.

Moving forward, the potential for significantly higher prices will come more from the global picture, rather than domestic. Brazil, Argentina, Ukraine, and the US typically account for 85% to 87% of global corn exports. Combined ending stocks for the 2021/22 marketing year are expected to be the tightest since 2012/13 at 1.86 billion bushels (fig. 6). This is a problem because demand for global imports is nearly double what they were in 2012/13. This leaves very little room for production shortfalls.

Brazil’s safrinha corn crop is almost totally planted, and La Nina remains a major concern in South America. Unlike last year, however, conditions appear to be much better. Rains are seemingly consistent, and more is on the way. Brazil's government said that the country's fertilizer stocks should last until October, although shortages associated with the Russia-Ukraine situation may present problems. Brazil imports most of its fertilizer products from Russia, China, Morocco, and Canada.

Depending on who you ask, Ukraine is planning to plant their corn crop on time. Yet, no one really knows if they have the resources to do so. Conflicting reports are making it difficult to pinpoint whether we can expect Ukraine to meet global corn needs